Hecht Insurance Advisors, LLC Blog |

The specter of having a severe illness or injury that requires long-term care is a scary proposition for most anybody, not to mention the financial obligations you would face. But trying to time when is the best age to purchase a policy is not an easy decision. Obviously, you don't want to buy the policy too early and unnecessarily spend thousands of dollars on premium over your life for coverage you may not need until you are much older. The younger you are when you buy a policy, the lower your premiums. That said, people typically do not purchase long-term care policies in their 30s or 40s since they are looking at a long time-horizon for when they would need to file a claim. After all, the policy may not be needed for 30 years or more. At the same time, if you wait until you are in your late 60s or early 70s, the premiums may be cost-prohibitive for you - not to mention you may have trouble finding an insurer willing to write your policy. For example, based on the "Genworth 2019 Cost of Care Survey," if purchased today, a long-term care policy with a maximum daily benefit of $150 a day for three years would cost an estimated:

As you can see, the ideal time cost-wise is probably in your 50s and 60s. But before pulling the trigger, you should think about how the premiums fit into your life and other obligations. If you have children who have not yet graduated from college, they will be your major concern. You should carry enough life insurance to see them through. But after your children, if any, are on their own, you might take the funds you were using to pay for life insurance premiums and use them to finance long-term care insurance premiums instead. What policies cover Long-term care insurance covers:

When shopping for a policy, you will have many choices to make: The trigger - Policies will have a trigger for when payments can commence. Often, policies base qualification on cognitive impairment or the need for assistance in at least two activities of daily living (dressing, toileting, eating, transferring, bathing and continence). Inflation riders - As you know, health care inflation is never-ending. While $150 may be sufficient to cover your cost of care today, that may not be the case in a decade or 20 years from now. With long-term care insurance, you often have the option to buy an inflation rider with the policy, which will increase the allowance for daily benefits by a certain percentage a year, like 5% on a flat or compound basis. But, you need to know that this type of rider comes with a price in increasing premiums. Some experts recommend that buyers aged under 70 purchase an inflation rider, while anybody older than 70 does not need to do so. Elimination period - The elimination period is the time the insured must wait before the policy starts paying out. During that period of waiting, you will be on the hook for long-term care expenses. Typically, the waiting period is anywhere from one to 90 days, but it could be even longer. The longer the elimination period, the lower the premium. That said, the premium savings you achieve by choosing a longer elimination period may not be worth it for you. Don't fall into the disclosure trap One thing you have to be very careful about when applying for long-term care insurance is full disclosure about your pre-existing conditions or prior illnesses. If you fail to tell the insurer about an illness, the company may refuse you coverage at the time you file for benefits. It's in your best interest to be upfront about your health, as you would rather be denied during the application process than have your claim denied after paying your premiums for years. There are other options available: There are life and annuity products with long-term care options available depending on your health, age, and resources that can work well too. Ready find solutions to your long-term care needs?

0 Comments

Adult Children on Your Policies Can Create Coverage Gaps

Homeowner's insurance

Under a homeowner's policy, the insured is limited to:

This causes issues for some people, as many children are still in college beyond the policy cut-off date. You could run into coverage gaps for their contents and personal liability if:

The picture gets murkier these days as well because many parents are renting an apartment or buying condos for their adult children to live in. Some parents may mistakenly think that since they are footing the bill, their insurance may still cover their adult child. But that's not the case. Auto coverage Typical auto insurance policies will include family members under the coverage. The standard policy form defines a family member as "a person related to you by blood, marriage or adoption who is a resident of your household." For your adult child's vehicle, insurance coverage is determined by:

As you can see, even if a parent owns the title of the car and it's insured under the parent's policy, if the adult child is driving the vehicle and lives on their own, they could run into coverage issues in certain instances. The following scenarios could leave you with coverage gaps:

If you have an adult child on your policy, play it safe and give us a call so we can go over your policy and circumstances with you to identify any possible coverage gaps. Without the proper insurance protection for injuries and damages, you risk significant financial liabilities that you may not be able to cover. Getting All the Facts for Your Estate Planning

The threshold for lifetime gift and estate tax increased - In 2020, the amount has risen to $11.58 million for individuals; it is $22.8 million for couples. This is the maximum amount of gifting via money or asset transfer allowed during a person's lifetime without tax consequences. The limit more than doubled in 2019 after tax legislation was signed into law by President Trump.

The annual gift exclusion amount is $15,000 - The annual federal gift tax exclusion allows you to give away up to $15,000 ($30,000 for couples) in 2019 to as many people as you wish, without those gifts counting against your $11.58 million lifetime exemption. Some types of gifts are not subject to this limit. For example, gifts to a spouse, a medical fund or an education fund are not included. Also, education and medical gifts are not taxable. When making medical or education gifts, transfer the funds directly to the institution rather than sending them to an individual recipient. Lifetime exclusion amount portability is still an option - Estate tax laws started allowing surviving spouses to use remaining lifetime exclusion amounts of their deceased spouses in 2011. In addition to simplifying estate planning, this gave couples a way to access exclusion amounts. Couples can transfer up to $22.8 million of their taxable property to their heirs without estate tax penalties. However, transfers must be made by election in the estate. The gift and estate tax effective rate is 40% - If your estate is under $11.8 million, congratulations: The federal estate tax will not apply to your estate. Any amounts over that threshold will be taxed at marginal tax rates that cap out at 40% for an estate worth more than $1 million over the cap. Remember state gift tax laws - While the rules covered in the previous sections apply to federal laws, they do not apply to state laws. Many states have laws that require estate and gift taxes. If the taxes include lifetime exclusion limits, they will be lower than the federal limits. To learn about individual state laws, discuss concerns with an agent. It is not possible to avoid these taxes in the states where they are required. The takeaway While estate planning is not something most people think about often, it should be considered every year - and when any major life changes happen. A new addition to a family, a marriage, a death in the family, getting a major promotion and big health changes are just a few examples of times when estate plans should be reviewed and changed as necessary. Neglecting these changes can cost a person's heirs a considerable amount of time and money. Stay on top of these issues to keep plans running smoothly. Call us 540-712-2199 to learn more about optimizing estate planning. Employers Guide for Dealing with the Coronavirus

On top of that, if you have workers who come down with the virus, you will need to consider how you're going to deal with sick leave issues. Additionally, workers who are sick or have family members who have stricken, may ask to take time off under the Family Medical Leave Act.

Coronavirus explained According to the Centers for Disease Control, the virus is transmitted between humans from coughing, sneezing and touching, and it enters through the eyes, nose and mouth. Symptoms include a runny nose, a cough, a sore throat, and high temperature. After two to 14 days, patients will develop a dry cough and mild breathing difficulty. Victims also can experience body aching, gastrointestinal distress and diarrhea. Severe symptoms include a temperature of at least 100.4ºF, pneumonia, and kidney failure. Employer concerns OSHA - OSHA's General Duty Clause requires an employer to protect its employees against "recognized hazards" to safety or health which may cause serious injury or death. According to an analysis by the law firm Seyfarth Shaw: If OSHA can establish that employees at a worksite are reasonably likely to be "exposed" to the virus (likely workers such as health care providers, emergency responders, transportation workers), OSHA could require the employer to develop a plan with procedures to protects its employees. Protected activity - If you have an employee who refuses to work if they believe they are at risk of contracting the coronavirus in the workplace due to the actual presence or probability that it is present there, what do you do? Under OSHA's whistleblower statutes, the employee's refusal to work could be construed as "protected activity," which prohibits employers from taking adverse action against them for their refusal to work. Family and Medical Leave Act - Under the FMLA, an employee working for an employer with 50 or more workers is eligible for up to 12 weeks of unpaid leave if they have a serious health condition. The same applies if an employee has a family member who has been stricken by coronavirus and they need to care for them. The virus would likely qualify as a serious health condition under the FMLA, which would warrant unpaid leave. What to do Here's what health and safety experts are recommending you do now:

If you have an employee you suspect has caught the virus, experts recommend that you:

If there is a massive outbreak in society, consider whether or not to continue operating. If you plan to continue, put a plan in place. You may want to:

Five Smart Things You Can Do with Life Insurance Cash Value

Stay put -Let life insurance be life insurance. Your money is growing tax-deferred within the policy. And in the event of your death, an amount much greater than your current cash value will generally pass to your heirs, tax-free.

That's a significant benefit right there, and a compelling reason not just to let your policy grow, but to add more premium to it if you can. Borrow against the death benefit - You can withdraw accumulated dividends, and then borrow against the rest of it, generally with no tax consequence, as long as you don't completely surrender the policy. Interest will accrue, but you don't have to repay the loan yourself unless you want to. If you don't pay it back, the insurance carrier will simply subtract the balance due from any death benefit they pay to your beneficiaries. Cash out the policy altogether - This option lets you get substantially all the cash in your policy. However, you may be subject to capital gains tax to the extent your cash value exceeds the amount you paid in. Exchange for another life insurance policy - If you choose, you can execute a Section 1035 exchange of one life policy for another, tax-free. You may opt to do this if you find ongoing premiums at a new carrier are lower for some reason, or if you want some specific protections or riders you can't get from your old carrier. For example, you may be able to exchange a straight-ahead universal or whole life insurance policy for a policy that also provides a benefit in the event you need long-term care insurance. Exchange for an annuity - You can also exchange a life insurance policy for an annuity, tax-free, under Section 1035. You might choose to do this if you decide you no longer want the life insurance protection, but you do want regular and reliable income. For example, if your beneficiaries are grown up and no longer rely on your life insurance death benefit, you may execute a 1035 exchange to a lifetime income annuity - maximizing your income over your expected lifetime, rather than paying a large death benefit. You can choose a joint and survivor annuity to guarantee income to your spouse as well. The takeaway Life insurance is among the most flexible and powerful resources you can have in your portfolio as you grow more established. But to have all of the above options later in life, you must plan ahead now. Talk to us today. We can help you develop a plan that meets your needs and financial objectives. Do You Know Your Flood Risk?

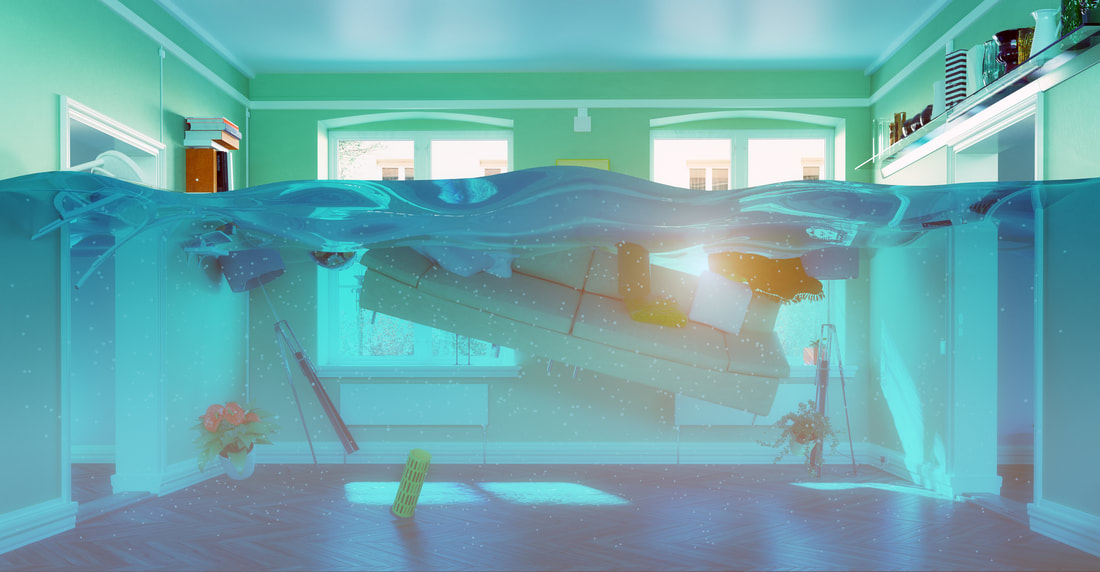

Gauging your flood risk

FEMA considers a property to be at high risk of flood if there is at least a one-in-four chance of flooding during the life of a 30-year mortgage. Geographic areas with this risk are known as special flood hazard areas (SFHAs). Federal regulations require federally regulated or insured mortgage lenders to confirm that mortgaged properties in these areas carry flood insurance. The traditional way to determine a property's flood risk is to locate it on a flood insurance rate map (FIRM). FEMA publishes these maps based on geographic survey data. They are the official depictions of flood hazards in a locality. FIRMs are freely available for review at the Flood Map Service Center on FEMA's website. As a property owner, you can view your flood risk by entering your address in the search field. Flood maps assign each area in a community to labeled flood zones. Areas with low-to-moderate risks of flooding are assigned to zones with labels beginning with the letters B, C, X or a shaded X. SFHAs are designated with the letters A or V. These areas are shaded on the maps for easy identification. Property owners can also search for their flood risks at FEMA's flood insurance consumer web site, www.floodsmart.gov. By entering your address in the fields on the home page, you can quickly learn whether you face a low-to-moderate or high risk. The site offers other valuable tools, such as an estimator that can calculate how much financial damage a given amount of water (two inches, four inches, etc.) would cause in homes of various sizes. For example, six inches of water in a 2,000 square foot home would cause $39,150 in damage. FEMA also offers a suite of flood risk products that go beyond the information provided in a FIRM. They include: • Flood risk maps, which show the overall picture of risk for a given area, • Flood risk reports, which show community-specific risk information, and • The Flood Risk Database, which stores all flood risk data for an area. These products are helpful for community planners, but individual property owners can also use them to get a clear idea of their flood risks. Elevation certificates may also be on file with local governments for certain properties. These documents show the elevation of the lowest floor of a building (including the basement) compared to the base flood elevation for the area. An elevation certificate demonstrates community compliance with flood-plain management laws and is used to set appropriate flood insurance premiums. The takeaway A flood can be every bit as catastrophic as a fire. It is worthwhile for property owners to learn their flood risk and take steps to reduce it. Additionally, with the increasing risk of flooding in non-flood-plain areas, if you live near a flood plain, you may want to secure flood insurance. 5 Ways You Can Maximize Your Social Security Benefits

Clearly, Social Security is not sufficient income for most of us by itself to fund an acceptable retirement lifestyle. But there are some things you can do to boost your monthly payout.

Controlling the Risks of Business VehiclesAs the cost of commercial auto insurance continues climbing at unprecedented rates, any business with vehicles has to make sure that it has procedures and policies in place to reduce the chances of its drivers causing accidents.

When a business entrusts a vehicle to an employee, it is literally putting its assets on the line. You should set these no-exception rules for drivers:

You should also set guidelines for employees to follow when they use company vehicles, such as: Limit their non-business use of vehicles - If employees take company cars home with them, you should set reasonable limits on personal use. Allow plenty of time between meetings and assignments - This will make it less necessary for employees to speed. Park vehicles wisely - Instruct workers to park vehicles in well-lit areas, and to lock them. Weeding out trouble You should also try to make sure that you don't put people in driving positions that are risky. You can:

But, even with all the preventive measures in the world, an accident will occasionally happen. You should prepare your drivers for that event. Develop procedures for what a worker should do after an accident. Keep copies of the procedures handy in vehicle glove boxes. Post-accident procedures

If one of your employees is involved in an accident, report the accident to us or your insurance company as soon as possible. Follow the conditions listed in the insurance policy. Check with us if you do not know what they are. Follow the insurer's instructions for getting repair estimates and communicating with physicians. Your insurance company may be able to help. Many insurers offer loss-prevention guidance for their customers. Businesses can reduce their risks and control their costs by working with their insurers and following the simple steps set out above.

With more cars connected to the web, helping us navigate, talking to other cars as we zoom down the road and sometimes even driving for us, it won't be long until our autos can also make an insurance claim for us after an accident.

Consider that more cars are being built with sensors and technology that allows them to communicate with external parties. It's not hard to imagine that the car could communicate immediately with emergency services and your insurance company if there is an impact. The emergency authorities could be notified in real time with detailed information about the condition of the vehicle and the location of the accident. Insurers are currently teaming up with tech firms and are developing programs that would prompt your vehicle to report immediately to your insurance company's data center if it's been in an accident, which could start the claim. These programs could also:

Right now, all of the technological parts of this puzzle are in place, and insurers are working with tech companies on apps to make it happen. Pioneering partnerships Insurance companies are also currently working to create partnerships with auto manufacturers to make all this a reality. The most notable of these partnerships involves General Motor's OnStar system, with the auto giant having secured relationships with about a half dozen auto insurance companies already in the US. In Europe, BMW and Allianz have a similar partnership. The evolution is ongoing, but in the next few years, as cars become smarter, it won't be long until we see the next stage in development for car insurance that will make your life easier and also give you an added sense of security. Renter's Insurance and Misconceptions among Millennials A recent study found that millennials are renting in larger numbers than ever before, but that they are not getting renter's coverage even though it's inexpensive and can provide protection for their belongings. Researchers also found that most (75%) of the people surveyed did not know they could obtain renter's insurance for about the same monthly cost as a pair of movie tickets, and had therefore not purchased coverage for their possessions. They concluded that there was a clear misconception among this group of young people about how important it is to have renter's insurance and the true cost of coverage. Leaving belongings at risk when about $20 per month can buy adequate coverage is an unwise move. Renters often live in properties with multiple units, and they may not always realize how high the risk of fires and other disasters are in these places. Although property owners are responsible for repairs to the structure in the event of most disasters, they are not responsible for tenants' belongings. It is up to renters to make sure their possessions are protected. In their research, experts also found that about 40% of people without renter's coverage did not think it was necessary. Nearly 70% of all young adult renters replied that the cost to replace all of their belongings would exceed $5,000. Renters who had coverage said they bought policies because they wanted the peace of mind to know they were protected. Renters' biggest fears:

Inexpensive peace of mind A plan that costs around $300 a year generally covers up to $50,000 worth of property. But most people won't need that much coverage as renters. A policy that covers $15,000 to $20,000 worth of property should be enough for most millennials. Such policies can sometimes be had for less than $200 a year, or as little as $10 to $15 a month. (The average renter's insurance premium cost about $187 in 2017, according to the Insurance Information Institute.) Renter's insurance is quick and easy to buy, and millennials everywhere should make sure they always have it. To learn more about this type of coverage and how affordable it is, call us today. |

Contact Us(540) 712-2199 Archives

May 2023

Categories

All

|

RSS Feed

RSS Feed