Hecht Insurance Advisors, LLC Blog |

How Having a Dog Can Benefit Your Health

More exercise - When you own a dog, you should be taking it out for walks every day. And the benefit is that when you're exercising your pooch, you too are exercising. Walking 30 minutes a day can do wonders for your health.

Less stress - Numerous studies have shown that people with dogs have lower stress levels. Engaging with your dog in whatever form can reduce your stress. Illness detection - Dogs really see the world through their noses thanks to their keen sense of smell. Some dogs are sensitive enough to detect the onset of epileptic seizures, or the presence of some cancers. Many dog owners have reported their dog sniffing, licking or nudging areas of the body that later turned out to be cancerous. More allergy tolerance - Children who are raised around pets have a reduced chance of having allergies. And growing up with a dog can boost immunity to pet allergies later in life. Boosting brain development - Dogs boost brain development in children, along with emotional growth and connection to others. Stronger heart - Studies have shown that petting a dog can lower your heart rate, and male pet owners tend to have reduced rates of heart disease. Less chance of depression - Dog owners are less likely to be depressed. The companionship they offer has been shown to help people who have been diagnosed with clinical depression, largely because caring for another living thing can help relieve symptoms of depression and make people feel more positive. Safety - Dogs are like a living alarm system. Barking dogs can keep burglars at bay and they can alert you if someone is snooping around the outside of your house, giving you a greater sense of security.

0 Comments

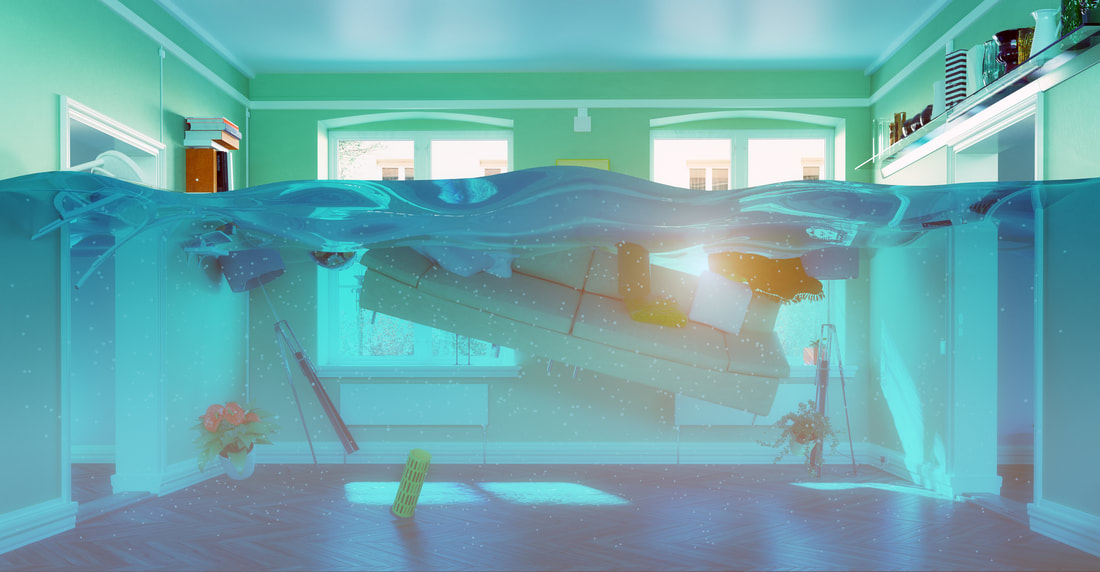

Homeowner's Insurance Issues during Coronavirus Outbreak

Here's what you should know about your homeowner's insurance at this time. Business at home If you have had to move your business to your home, you may want to review your homeowner's coverage. The typical homeowner's police have very low limits on business property (usually up to about $2,000), which would likely not be enough if your equipment is damaged or stolen. If you are suddenly running your business from home, please call us and we can go through your policy and, if needed, we can work with your insurer to see if they offer a home business endorsement or higher coverage limits for business property. Also, if you are running an Airbnb out of your home for a room or another property, you should have purchased landlord coverage or home-sharing coverage as a typical homeowner's policy may not cover damage incurred by paying guests. At this time, you are likely not getting anybody staying at your place, so you should contact your insurance company about pausing or canceling coverage since you will have no need for it for a while. Filing a claim If you have an incident in your home and need to file a claim, there's a good chance that your insurer will be unable to send an adjuster for an inspection. Most homeowner's insurers now have apps or offer you the ability to file your claim online on their website. The procedures for filing a claim using an app or doing it on your insurer's website is pretty straightforward. You can start by taking pictures of the damage and providing receipts or a list of the property that may have been damaged or stolen. If it was stolen, make sure you file a police report and submit that with the claim as well. However, if you have a high-dollar claim, the insurer may send an adjuster to inspect the damage before they pay the claim. For smaller claims, it's likely they will pay them out. What insurers are doing Insurers are making adjustments to their operations and policies during this time as well. Their actions will vary from company to company, but there are similarities in some of their responses:

Smart Home Sensors Can Save You from Calamity

You can set up some smart sensors as stand-alone units with their own dedicated hub, while others are adaptable and can communicate with brand-name smart home hubs like:

The sensors communicate with a central hub using Bluetooth technology, while the hub uses your home Wifi to alert the app on your phone. Here are the sensors that can give you the most bang for your buck in terms of safety and preventing damage to your home, its contents, your family - and even pets. Water sensors There are a number of smart leak detectors on the market, and depending on the brand, the system can shut off water in about five seconds after detecting a leak in your home. This can save you thousands of dollars in property damage. You can place these sensors at specific points where leaks are possible, such under sinks, appliances and water heaters. This allows you to customize a leak detection solution based on your needs or concerns. Some sensors can even detect changes in water temperature, which can help you avoid damage from frozen pipes. These sensor units may also include shut-off valves, which can be installed at strategic locations in your piping. It's best to call a plumber because installing a shut-off valve may require cutting into the water line. Leave that to the pros. Freeze sensors These are typically only necessary in regions that have freezing temperatures and snow for periods of time in the winter. When pipes freeze, they can back up, expand and burst and possibly flood parts of your home. Many of the systems that detect leaks also can detect if pipes have frozen. Like leak sensors, freeze sensors are small devices that constantly monitor the temperature of the object or area they're in touch with. If a sensor detects frozen pipes, it will notify you via your smart phone app or activate a shut-off valve if it's installed. Smart smoke alarms A smart smoke alarm works just like a normal smoke alarm, except it has the added feature of notifying you if there is a fire and you are not home. That gives you the opportunity to call the fire department or a trusted neighbor to ensure a faster response. If you own an Alexa speaker, it has a feature that will act as a smoke alarm by listening for the sound of your regular smoke alarm then send you an alert. There is also a smart 9V battery on the market that you plug into your smoke alarm and which alerts you in case it goes off. Temperature sensors Smart temperature sensors can alert you to changes in areas of your home that need to have steady temperatures, such as wine cabinets, crib rooms, pet enclosures and humidors. Window and door sensors For your home security needs, you may want to consider door and window sensors. They usually come in two parts - one that attaches to the door or window frame, and another that attaches to the door or window itself. When the door or window is closed, the circuit between the two parts of the sensor is complete and so is marked as 'closed' - but as soon as a door or window is opened, the circuit is 'broken,' which triggers an alert. Adult Children on Your Policies Can Create Coverage Gaps

Homeowner's insurance

Under a homeowner's policy, the insured is limited to:

This causes issues for some people, as many children are still in college beyond the policy cut-off date. You could run into coverage gaps for their contents and personal liability if:

The picture gets murkier these days as well because many parents are renting an apartment or buying condos for their adult children to live in. Some parents may mistakenly think that since they are footing the bill, their insurance may still cover their adult child. But that's not the case. Auto coverage Typical auto insurance policies will include family members under the coverage. The standard policy form defines a family member as "a person related to you by blood, marriage or adoption who is a resident of your household." For your adult child's vehicle, insurance coverage is determined by:

As you can see, even if a parent owns the title of the car and it's insured under the parent's policy, if the adult child is driving the vehicle and lives on their own, they could run into coverage issues in certain instances. The following scenarios could leave you with coverage gaps:

If you have an adult child on your policy, play it safe and give us a call so we can go over your policy and circumstances with you to identify any possible coverage gaps. Without the proper insurance protection for injuries and damages, you risk significant financial liabilities that you may not be able to cover. Do You Know Your Flood Risk?

Gauging your flood risk

FEMA considers a property to be at high risk of flood if there is at least a one-in-four chance of flooding during the life of a 30-year mortgage. Geographic areas with this risk are known as special flood hazard areas (SFHAs). Federal regulations require federally regulated or insured mortgage lenders to confirm that mortgaged properties in these areas carry flood insurance. The traditional way to determine a property's flood risk is to locate it on a flood insurance rate map (FIRM). FEMA publishes these maps based on geographic survey data. They are the official depictions of flood hazards in a locality. FIRMs are freely available for review at the Flood Map Service Center on FEMA's website. As a property owner, you can view your flood risk by entering your address in the search field. Flood maps assign each area in a community to labeled flood zones. Areas with low-to-moderate risks of flooding are assigned to zones with labels beginning with the letters B, C, X or a shaded X. SFHAs are designated with the letters A or V. These areas are shaded on the maps for easy identification. Property owners can also search for their flood risks at FEMA's flood insurance consumer web site, www.floodsmart.gov. By entering your address in the fields on the home page, you can quickly learn whether you face a low-to-moderate or high risk. The site offers other valuable tools, such as an estimator that can calculate how much financial damage a given amount of water (two inches, four inches, etc.) would cause in homes of various sizes. For example, six inches of water in a 2,000 square foot home would cause $39,150 in damage. FEMA also offers a suite of flood risk products that go beyond the information provided in a FIRM. They include: • Flood risk maps, which show the overall picture of risk for a given area, • Flood risk reports, which show community-specific risk information, and • The Flood Risk Database, which stores all flood risk data for an area. These products are helpful for community planners, but individual property owners can also use them to get a clear idea of their flood risks. Elevation certificates may also be on file with local governments for certain properties. These documents show the elevation of the lowest floor of a building (including the basement) compared to the base flood elevation for the area. An elevation certificate demonstrates community compliance with flood-plain management laws and is used to set appropriate flood insurance premiums. The takeaway A flood can be every bit as catastrophic as a fire. It is worthwhile for property owners to learn their flood risk and take steps to reduce it. Additionally, with the increasing risk of flooding in non-flood-plain areas, if you live near a flood plain, you may want to secure flood insurance. Home SharingThe sharing economy is projected to grow from $15 billion in 2014 to $335 billion in 2025. Even though some localities have enacted regulations to curb this sector, it continues its rapid growth. Unfortunately, people getting into this market space do not realize the underlying risks until it’s too late.

Are you renting out part or all of your home on a home-sharing site like Airbnb? Then proper insurance protection becomes a more intricate and complicated. Many mistakenly believe that a traditional homeowners policy is all the insurance protection they need. Many people fail to recognize that by accepting rental income, their homes have been turned into a business. Without appropriate insurance a significant portion of your personal assets can be at risk. Home-sharing has implications for all parties involved: the host, who may own or rent the listed property; the host’s landlord, if the listed property is rented by the host; the guest, who books a stay through the home-sharing site; and the home-sharing company, which connects hosts with guests. Not only guests, but hosts as well could incur costs if things go awry. Even if hosts take preventive measures, someone could trip over a rug or slip on a wet floor, causing injury. Accidents can and do happen anytime, anywhere. If you own a home or even rent a home, it is important to cover your personal property and protect yourself from the liability and consequences of litigation in the event that someone is seriously injured or even dies on your property. Lawyers will not only go after the home-sharing company policy, that you think protects you; but also the homeowners and property owners as well. Did you know that if you don’t disclose your home sharing activities to your insurer that you could be subject to policy cancellation, even retroactively, if you don’t get caught until you need to file a claim? It is critical that you do your research and work with your insurance agent before jumping on the home sharing bandwagon. Even if you are renting your home just once, once is all it takes. You can’t afford to jeopardize your coverage or your family's financial security. |

Contact Us(540) 712-2199 Archives

May 2023

Categories

All

|

RSS Feed

RSS Feed