Hecht Insurance Advisors, LLC Blog |

Do You Know Your Flood Risk?

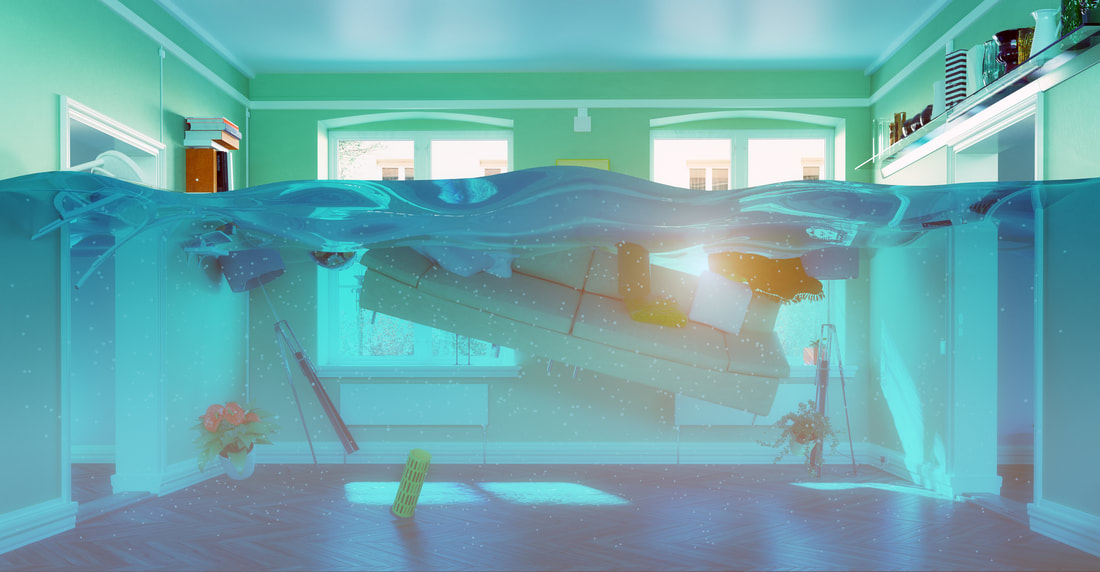

Gauging your flood risk

FEMA considers a property to be at high risk of flood if there is at least a one-in-four chance of flooding during the life of a 30-year mortgage. Geographic areas with this risk are known as special flood hazard areas (SFHAs). Federal regulations require federally regulated or insured mortgage lenders to confirm that mortgaged properties in these areas carry flood insurance. The traditional way to determine a property's flood risk is to locate it on a flood insurance rate map (FIRM). FEMA publishes these maps based on geographic survey data. They are the official depictions of flood hazards in a locality. FIRMs are freely available for review at the Flood Map Service Center on FEMA's website. As a property owner, you can view your flood risk by entering your address in the search field. Flood maps assign each area in a community to labeled flood zones. Areas with low-to-moderate risks of flooding are assigned to zones with labels beginning with the letters B, C, X or a shaded X. SFHAs are designated with the letters A or V. These areas are shaded on the maps for easy identification. Property owners can also search for their flood risks at FEMA's flood insurance consumer web site, www.floodsmart.gov. By entering your address in the fields on the home page, you can quickly learn whether you face a low-to-moderate or high risk. The site offers other valuable tools, such as an estimator that can calculate how much financial damage a given amount of water (two inches, four inches, etc.) would cause in homes of various sizes. For example, six inches of water in a 2,000 square foot home would cause $39,150 in damage. FEMA also offers a suite of flood risk products that go beyond the information provided in a FIRM. They include: • Flood risk maps, which show the overall picture of risk for a given area, • Flood risk reports, which show community-specific risk information, and • The Flood Risk Database, which stores all flood risk data for an area. These products are helpful for community planners, but individual property owners can also use them to get a clear idea of their flood risks. Elevation certificates may also be on file with local governments for certain properties. These documents show the elevation of the lowest floor of a building (including the basement) compared to the base flood elevation for the area. An elevation certificate demonstrates community compliance with flood-plain management laws and is used to set appropriate flood insurance premiums. The takeaway A flood can be every bit as catastrophic as a fire. It is worthwhile for property owners to learn their flood risk and take steps to reduce it. Additionally, with the increasing risk of flooding in non-flood-plain areas, if you live near a flood plain, you may want to secure flood insurance.

0 Comments

Home SharingThe sharing economy is projected to grow from $15 billion in 2014 to $335 billion in 2025. Even though some localities have enacted regulations to curb this sector, it continues its rapid growth. Unfortunately, people getting into this market space do not realize the underlying risks until it’s too late.

Are you renting out part or all of your home on a home-sharing site like Airbnb? Then proper insurance protection becomes a more intricate and complicated. Many mistakenly believe that a traditional homeowners policy is all the insurance protection they need. Many people fail to recognize that by accepting rental income, their homes have been turned into a business. Without appropriate insurance a significant portion of your personal assets can be at risk. Home-sharing has implications for all parties involved: the host, who may own or rent the listed property; the host’s landlord, if the listed property is rented by the host; the guest, who books a stay through the home-sharing site; and the home-sharing company, which connects hosts with guests. Not only guests, but hosts as well could incur costs if things go awry. Even if hosts take preventive measures, someone could trip over a rug or slip on a wet floor, causing injury. Accidents can and do happen anytime, anywhere. If you own a home or even rent a home, it is important to cover your personal property and protect yourself from the liability and consequences of litigation in the event that someone is seriously injured or even dies on your property. Lawyers will not only go after the home-sharing company policy, that you think protects you; but also the homeowners and property owners as well. Did you know that if you don’t disclose your home sharing activities to your insurer that you could be subject to policy cancellation, even retroactively, if you don’t get caught until you need to file a claim? It is critical that you do your research and work with your insurance agent before jumping on the home sharing bandwagon. Even if you are renting your home just once, once is all it takes. You can’t afford to jeopardize your coverage or your family's financial security. |

Contact Us(540) 712-2199 Archives

May 2023

Categories

All

|

RSS Feed

RSS Feed